Nov 6, 2025

The Economics of Connectivity: Telecoms and Consumer Access in Africa

Much like roads, energy, and water systems, the telecommunications sector now underpins Africa’s modern economy. It enables digital trade, e-governance, education, and financial inclusion, serving as both an enabler and amplifier of growth.

According to the International Telecommunication Union (ITU), Africa’s mobile broadband subscription rate rose from 20% in 2015 to 52% in 2023, a remarkable leap in less than a decade.

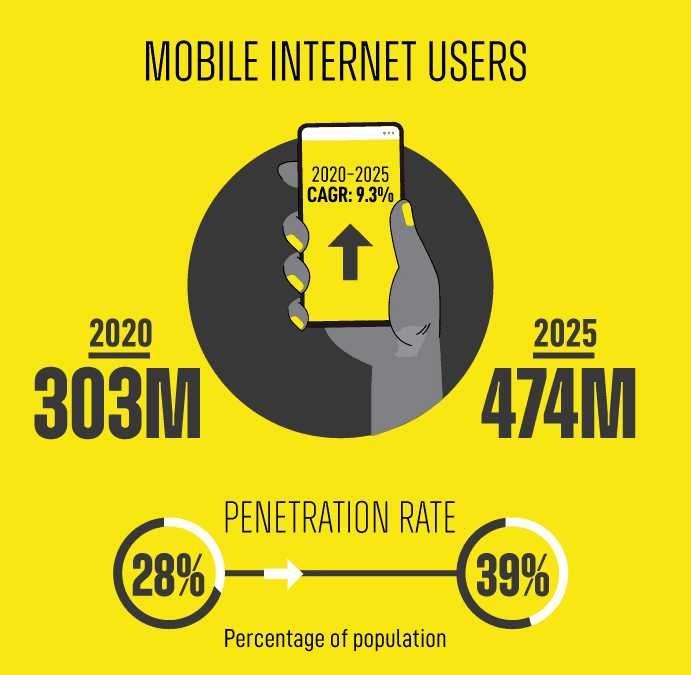

Yet challenges persist. Internet usage stood at 38% in 2024, far below the global average of 68%. This contrast captures the dual reality of Africa’s telecom landscape: rapid expansion coupled with persistent inequality. Nonetheless, the sector’s trajectory remains clear; telecoms have become the economic infrastructure of the digital era, forming the foundation for Africa’s next phase of sustainable and inclusive growth.

Rapid expansion and digital transformation

Africa’s connectivity transformation has unfolded at unprecedented speed. The convergence of affordable smartphones, expanding broadband coverage, and the accelerated rollout of 4G and emerging 5G networks has unlocked new economic potential. Connectivity now contributes over $170 billion annually to Africa’s GDP, empowering small enterprises, widening labour markets, and fueling innovation clusters in cities like Lagos, Nairobi, and Cairo.

This year, internet penetration is expected to exceed 40%, with the continent’s digital economy projected to add nearly $180 billion to GDP. Telecom networks have evolved from communication infrastructure into strategic economic assets, driving inclusion, productivity, and innovation.

Telecoms as core infrastructure in the global economy

Globally, telecommunications have transitioned from a service industry to a critical national infrastructure. According to PwC’s Global Telecoms Outlook (2023), the sector reached $1.1 trillion despite inflationary pressures. For emerging economies, fixed broadband and wireless networks now form the backbone of digital competitiveness.

In Africa, investments in fibre networks and Fixed Wireless Access (FWA) are helping bridge the urban–rural divide. These technologies are vital for delivering high-speed connectivity to underserved areas, ensuring that digital participation extends beyond metropolitan centres.

The mobile sector: Africa’s growth engine

The GSMA’s Mobile Economy Africa 2025 report identifies mobile telecommunications as both a social lifeline and a growth driver. The industry contributed US$220 billion (7.7% of GDP) in 2024 and is projected to reach US$270 billion by 2030.

However, systemic challenges remain. A 2GB mobile data plan still costs an average of 4.2% of GNI per capita, double the UN’s affordability target. While 4G networks cover 71% of Africa’s population, global coverage stands at 92%. 5G access remains limited to 11%, concentrated in urban hubs. These disparities underline the need for targeted infrastructure investments and policy alignment to sustain equitable connectivity.

Côte d’Ivoire: A model for telecom-led development

Côte d’Ivoire illustrates how telecom investments translate into economic growth. Between 2019 and 2023, national telecom revenue expanded by nearly 30%, reaching CFA 1.219 trillion (US$2 billion), driven by rapid fibre rollout and 4G coverage reaching 94% of localities.

Under the National Digital Development Strategy (2021–2025), telecom expansion is projected to yield $5.5 billion in returns by 2025 and more than $20 billion by 2050. Similar patterns are emerging across Africa, confirming telecommunications as a pillar of productivity, employment, and GDP growth.

The persistent divide: Access and affordability

Despite remarkable progress, connectivity remains uneven. Major cities such as Lagos, Nairobi, and Accra are thriving as digital innovation hubs, yet millions in rural and low-income regions remain offline. Limited access to affordable data, devices, and stable electricity has created a structural divide that constrains participation in education, healthcare, e-commerce, and civic life.

For many households, the internet is out of budget rather than out of reach. Fixed broadband costs average 15% of GNI per capita, making it inaccessible to most rural users. Smartphones, now the primary tool for connectivity, can cost up to 30% of monthly income once import taxes and distribution margins are included.

The cost of staying connected

Even when connectivity is in place, sustaining it remains costly. High data prices, power instability, and indirect costs such as travel to digital service points create daily barriers. With over 600 million Africans lacking access to electricity, connectivity is often intermittent, devices remain uncharged, networks are unreliable, and community digital hubs are frequently disrupted.

These structural bottlenecks underscore that connectivity requires more than coverage; it demands affordability, reliability, and integration with broader infrastructure systems such as energy and transport.

Digital literacy: Enabling inclusive participation

Access without digital literacy yields limited inclusion. In many marginalised communities, training opportunities are scarce or unaffordable. Digital upskilling programs often require fees, transport, or time away from work — costs many cannot absorb.

This skills gap perpetuates inequality: those who can afford to learn benefit disproportionately from digital tools, while others remain excluded. Building inclusive digital skills ecosystems through community training, mobile learning, and public–private partnerships is therefore critical to unlocking full participation in the digital economy.

Signs of progress

Encouraging progress is emerging across the continent. According to the 2025 Global Relocate Internet Cost Ranking, Malawi, Nigeria, and Ghana now rank among the top 50 nations for low-cost mobile data, with average prices below $0.50 per gigabyte.

2025 Global Relocate Internet Cost Ranking

Country | Global Rank | Mobile Data Price (USD) | Internet Speed (Mbps) |

Malawi | 30 | 0.38 | 21.94 |

Nigeria | 31 | 0.39 | 25.79 |

Ghana | 33 | 0.40 | 13.59 |

Somalia | 45 | 0.50 | 16.08 |

Rwanda | 50 | 0.55 | 18.10 |

Kenya | 55 | 0.59 | 23.68 |

Morocco | 58 | 0.63 | 39.04 |

Egypt | 61 | 0.65 | 25.11 |

Mauritius | 66 | 0.67 | 49.66 |

DRC Congo | 67 | 0.68 | 17.00 |

These gains are attributed to regulatory reforms, competitive market structures, and infrastructure-sharing initiatives that enhance efficiency and reduce costs. Several countries are also reviewing spectrum taxation policies to align fiscal frameworks with universal access objectives.

Toward universal and affordable connectivity

Closing Africa’s connectivity and affordability gap demands coordinated, multi-stakeholder action. Governments must adopt tax and spectrum policies that prioritise access over revenue extraction. Telecom operators should pursue inclusive business models that balance profitability with affordability, while international partners can support this by financing infrastructure, subsidising devices, and investing in digital literacy.

Treating connectivity as a public good rather than a private commodity is the key to achieving universal access. Only through affordability, inclusivity, and policy coherence can Africa realise its vision of a digitally integrated and economically empowered continent.

More Insight from Real Life Users

Insights that Drive Change

Empowering smarter decisions across business, policy, and research